Recognition programs rarely fail because employees dislike them.

They stall because finance can't get comfortable with the tax implications.

It follows a predictable sequence. HR wants to launch or expand a recognition program. Finance asks whether gift cards are taxable. Payroll asks how points redemptions should appear on W-2s. Procurement asks who owns compliance reporting. Nobody has a clear answer, the evaluation slows down, and what started as an employee experience initiative turns into a tax governance discussion.

This post exists to make that conversation easier and shorter.

The IRS rules around employee recognition aren't complicated once you see the framework. The rules are scattered across multiple tax provisions, rarely explained in HR-readable language, and almost never built into how recognition platforms work. Most organizations don't find these gaps during program design. They find them during payroll reconciliation, vendor implementation, or an audit.

This is where most recognition programs discover whether they were designed for engagement, or designed for governance too late.

Key Takeaways

- Why Recognition Taxation Has Become a Buying-Cycle Issue

- The IRS Framework: Not All Recognition Is Treated Equally

- De Minimis: The Rule That Breaks Down at the Gift Card Counter

- Gift Cards: Disproportionate Risk, Consistent Misunderstanding

- Points-Based Programs: The Taxable Event Is at Redemption, Not Accumulation

- Peer-to-Peer Recognition: The Employer Always Owns the Reporting

- Service Awards: The §274(j) Exemption Most Programs Leave on the Table

- W-2 Reporting: Where Culture Strategy Meets Operational Execution

- Where Recognition Programs Usually Break Down

- What to Ask Your Recognition Vendor

- The Rules, Plainly

Why Recognition Taxation Has Become a Buying-Cycle Issue

A decade ago, recognition programs were relatively simple. A service award here. A holiday gift there. Spot bonuses processed through payroll. Tax handling was straightforward because the programs were.

That is no longer the case.

According to Vantage Circle's AIRe Benchmarking Report, organizations have moved away from periodic rewards toward continuous recognition: peer-to-peer nominations, instant redemptions, points economies, milestone automation, and global rewards catalogs all running at once. Recognition became always-on. Tax handling didn't keep pace.

The result: what once sat quietly in payroll as a footnote now pulls HR, finance, payroll, and procurement into the same room. Most of those conversations still happen without a clear framework to guide them.

The deeper shift is that recognition programs are no longer operating as lightweight culture initiatives. They increasingly sit inside broader compensation, retention, and employee experience ecosystems, which means finance scrutiny was always going to follow eventually.

The IRS Framework: Not All Recognition Is Treated Equally

The biggest misconception in employee recognition tax is assuming all awards work the same way. They don't. The IRS evaluates recognition based on what was given, why it was given, how it was delivered, and whether it functions like compensation. Most programs fall under two provisions.

IRC §132(e): De Minimis Fringe Benefits covers small, infrequent non-cash benefits that are administratively impractical to track. Classic examples: a holiday turkey, occasional event tickets, office snacks. Cash and cash equivalents are explicitly excluded, meaning gift cards, prepaid cards, and points redeemable for cash-equivalent rewards can never qualify as de minimis benefits, regardless of their value.

IRC §274(j): Employee Achievement Awards creates a narrow but real tax exclusion for service awards and safety achievement awards, with strict qualification rules around award type, employee eligibility, presentation format, and annual dollar limits.

Everything outside these two categories is ordinary taxable compensation, subject to withholding, FICA, and W-2 reporting. Knowing which bucket your program falls into before launch is what separates a scalable strategy from a compliance problem that surfaces three years later.

De Minimis: The Rule That Breaks Down at the Gift Card Counter

The de minimis rule is among the most misapplied provisions in employee recognition. Most HR teams assume that small-value awards don't need to be reported because the amount feels insignificant. The IRS doesn't evaluate it that way.

The de minimis exclusion exists because of administrative impracticality. If tracking a small, infrequent, non-cash benefit would create unreasonable administrative burden, the IRS may allow it to be excluded from taxable income. That reasoning holds for a birthday cake or a bouquet of flowers. It breaks down the moment a reward starts to resemble cash.

Gift cards, digital wallets, prepaid balances, and cash-equivalent points don't qualify for de minimis treatment at any value. Cash-equivalent benefits are trackable by definition. You can't claim administrative impracticality for something with a clear dollar amount attached. A $10 coffee gift card distributed company-wide creates taxable income and W-2 reporting obligations for every single recipient. There is no floor below which a gift card becomes tax-free.

Most HR teams aren't intentionally creating compliance exposure here. Recognition often feels cultural. The IRS evaluates it economically. Those aren't always the same thing.

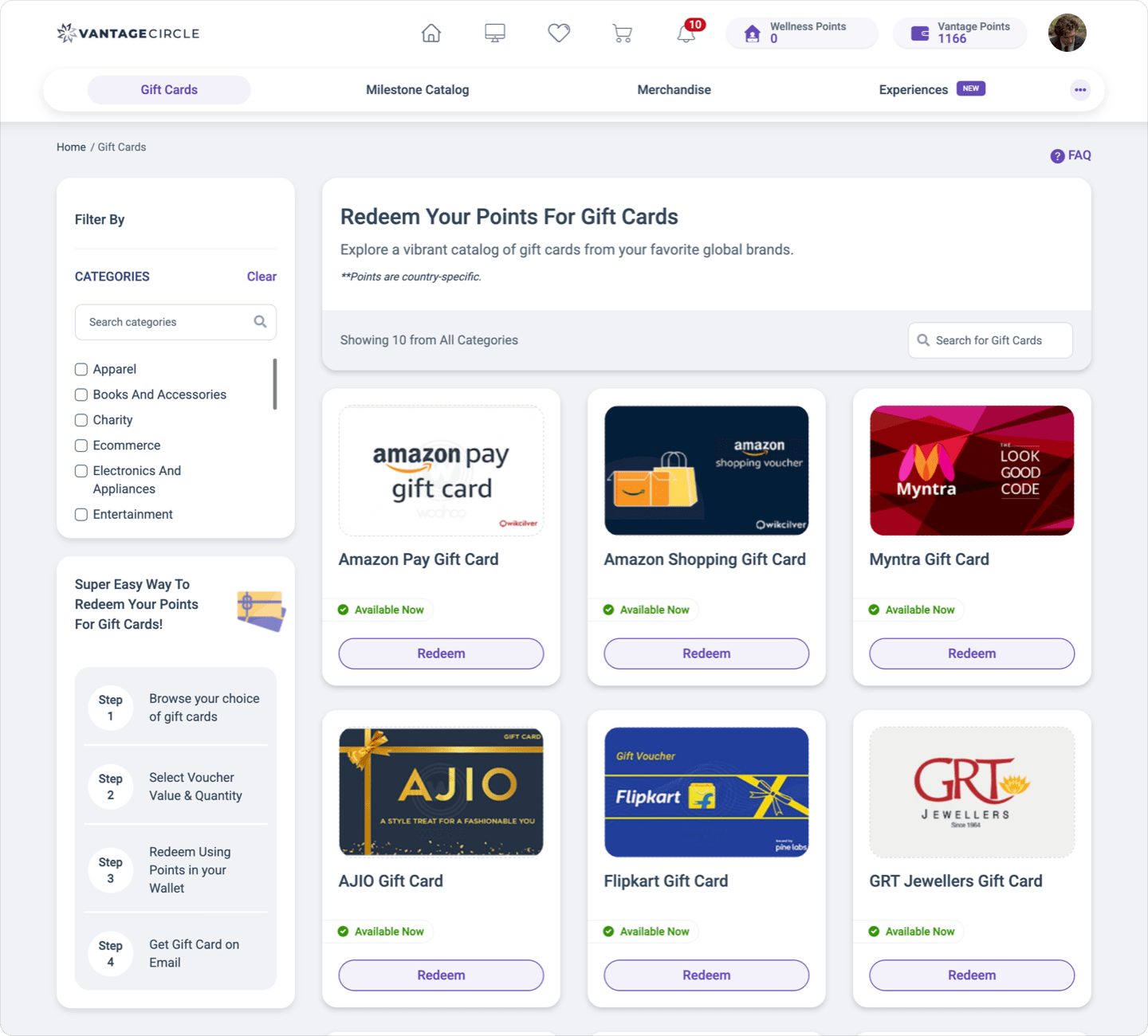

Gift Cards: Disproportionate Risk, Consistent Misunderstanding

Source: Vantage Circle — Rewards & Recognition Platform

Source: Vantage Circle — Rewards & Recognition Platform

Gift cards get their own section because the compliance risk here is disproportionate to how casually they tend to be used.

The IRS position is clear: gift cards are cash equivalents, taxable regardless of denomination, retailer, occasion, or delivery method. A $5 digital code is taxable. A retailer-specific card is taxable. The holiday appreciation cards your team distributed to every employee in December, taxable to every one of them. This is the position in IRS Technical Advice Memorandum 200437030 and it has held consistently.

From a payroll perspective, gift cards are supplemental wages. They require withholding at the 22% federal supplemental rate, W-2 reporting, and employer FICA handling. At scale, the numbers are concrete. Consider two companies, both spending $400 per employee to mark five-year milestones across 400 employees.

| $400 Amazon gift card | $400 engraved watch (§274(j) qualified) | |

|---|---|---|

| Supplemental wages | $160,000 | $0 |

| Employer FICA | ~$12,240 | $0 |

| W-2 line items | 400 | 0 |

Same budget. Structurally different outcome.

The rule itself isn't hard to understand. Recognition workflows and payroll workflows are usually built by different teams with different priorities. That gap is exactly where the liability accumulates.

Points-Based Programs: The Taxable Event Is at Redemption, Not Accumulation

When employees accumulate points in your recognition program, HR and payroll need to agree on one question: when does the tax obligation arise?

Under IRS guidance, informed by Announcement 2002-18 and subsequent application, the answer is redemption, not accumulation. Unredeemed points create no tax obligation. What becomes taxable is the fair market value of what the employee received at redemption, not the point balance they held.

That timing creates real operational pressure at scale. Large programs process thousands of redemption transactions across business units every month. If redemption data can't flow cleanly into payroll systems, year-end reporting doesn't just get complicated. It becomes a crisis.

IBS Software, operating across more than 20 countries including the US, built its program around this distinction, separating monetarily-backed redemptions from social recognition at the platform level rather than running everything through a single points ledger. Simpler administration, less tax exposure.

Your platform needs to clearly separate:

- Social recognition from points accumulation

- Taxable redemption activity from non-taxable interactions

- Gift card redemptions from merchandise redemptions

If your vendor can't produce that data in a format your payroll team can actually use, that gap has a cost. It just doesn't show up in the pricing proposal.

On the program design side: How to Start a Peer-to-Peer Recognition Program: A 3-Phase Playbook

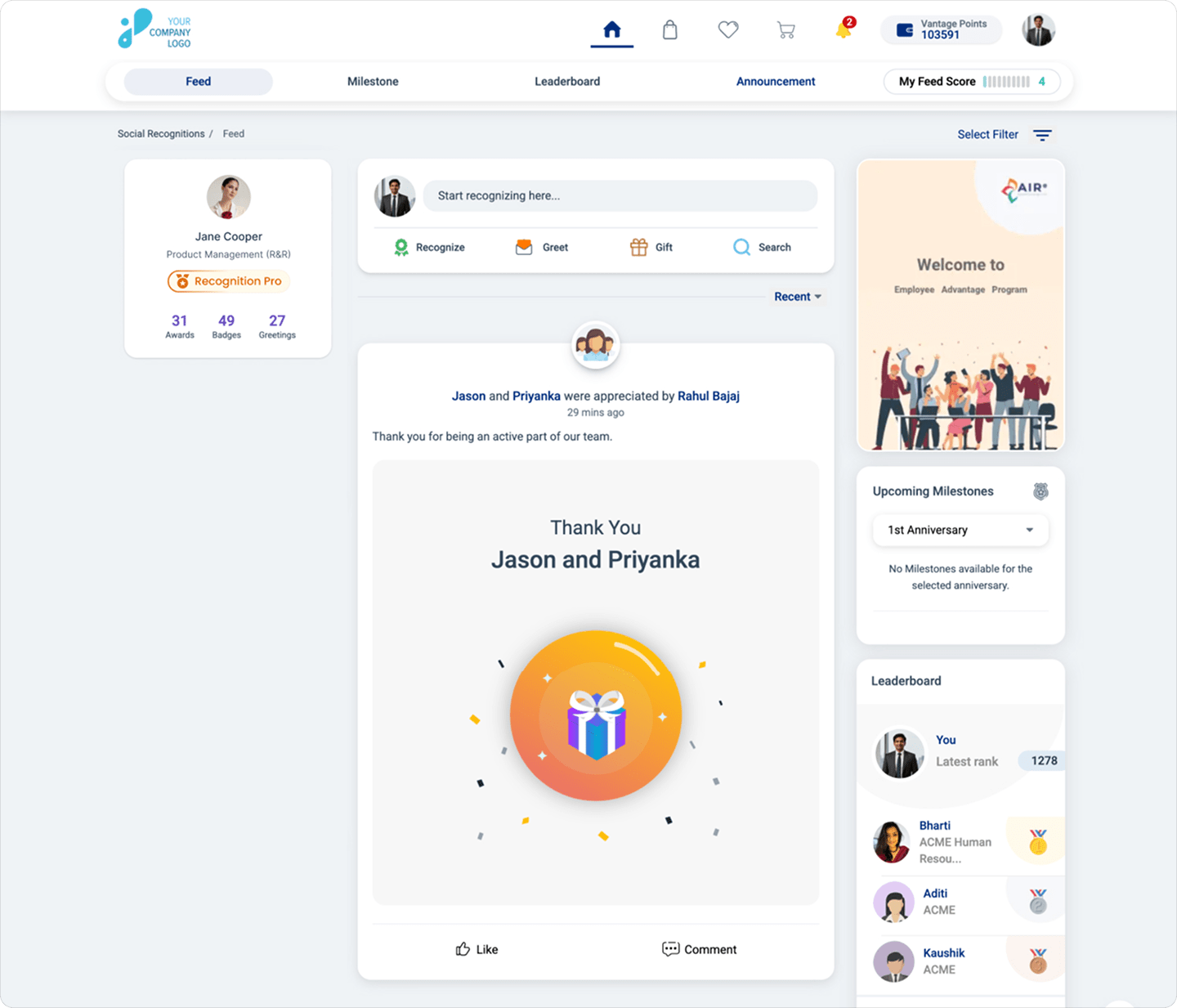

Peer-to-Peer Recognition: The Employer Always Owns the Reporting

Source: Vantage Circle — Rewards & Recognition Platform

Source: Vantage Circle — Rewards & Recognition Platform

If you fund the rewards, operate the platform, and enable redemption, you own the reporting obligation. It doesn't matter who initiated the recognition. For a broader look at how peer-to-peer recognition functions as a program design element, including how it drives participation and culture, that context is worth reading alongside the compliance picture here.

That surprises some teams. Because the recognition originates between employees, they assume the reporting obligation sits somewhere outside employer responsibility. It doesn't.

Modern platforms blend social recognition, monetary rewards, points systems, and redemption catalogs into a single employee experience. Social recognition with no monetary value is generally not taxable. The moment recognition carries redeemable economic value, payroll follows.

Platform architecture is a compliance decision, not just a product preference. A platform that can't separate social kudos from monetarily-backed awards in its reporting creates manual reconciliation work that compounds every time an employee hits the redeem button.

Service Awards: The §274(j) Exemption Most Programs Leave on the Table

Among all recognition categories, service awards offer the clearest opportunity for legitimate tax advantage, and it's consistently underused.

Under IRC §274(j), a length-of-service award given as tangible personal property in a meaningful presentation may be excluded from the employee's taxable income. Meaningful presentation is a distinct qualification requirement: the award must be given in a formal, documented context that acknowledges the achievement. Mailing the award or distributing it without any ceremony does not satisfy this standard, even when every other qualification criterion is met.

On the tax rules for service awards: Service Awards and Tax Benefits: What HR Needs to Know in the US and Canada

Exclusion limits:

- Up to $400 per employee per year under a non-qualified plan

- Up to $1,600 per employee per year under a qualified written plan

A qualifying award generally requires all of the following:

- Come after at least five years of service (first award), with subsequent awards at least five years apart

- Take the form of tangible personal property, not gift cards, cash, meals, travel, or securities

- Come from a plan that doesn't favor officers or employees earning above the HCE threshold ($160,000)

- Be documented in a formal written plan

The gap between $400 and $1,600 is entirely a documentation question. Many organizations unknowingly operate at the lower limit simply because their recognition plan was never written down.

For a full overview of how to structure years of service awards effectively, that post covers program design, milestone timing, and award formats in depth. While 74% of organizations have some form of service anniversary program (SHRM), most forfeit the §274(j) exclusion entirely by defaulting to gift cards or cash. Receiving a $1,600 engraved award under a qualified plan and receiving a $1,600 gift card may feel identical to an employee. The tax outcome is not. One may create no taxable income at all. The other creates taxable compensation plus employer payroll tax.

W-2 Reporting: Where Culture Strategy Meets Operational Execution

Every recognition program eventually reaches payroll. That is where the cultural intent of recognition meets the operational reality of compliance.

| Recognition Type | Taxable | W-2 Reportable |

|---|---|---|

| Cash awards | Yes | Yes |

| Gift cards | Yes | Yes |

| Points redeemed for merchandise | Yes | Yes |

| Points redeemed for gift card | Yes | Yes |

| Qualified service award §274(j) | Excess only | Excess only |

| Social recognition (no monetary value) | No | No |

| True de minimis non-cash items | Generally no | Generally no |

Source: Vantage Circle — Rewards & Recognition Platform

Source: Vantage Circle — Rewards & Recognition Platform

Two mechanics matter beyond the table. First, withholding: awards added to a regular payroll run are withheld at the employee's marginal rate. Standalone supplemental wage payments use the 22% flat rate for employees whose supplemental wages are below $1 million for the year. That is the flat-rate method, which applies when the award is paid separately from regular wages. If the award is combined with a regular paycheck, the aggregate method applies instead: withholding is calculated at the employee's effective rate based on their W-4, which typically produces a different number. For employees whose total supplemental wages exceed $1 million in a calendar year, withholding jumps to 37% regardless of method. This is uncommon for most recognition programs but worth noting for organizations running high-value awards for senior executives. Second, timing: the W-2 obligation falls in the calendar year the award is received or redeemed, not when it was earned or announced. Points redeemed in December belong on that year's W-2. Holiday gift cards distributed after payroll closes create an off-cycle run or a January true-up. Companies that treat year-end appreciation as outside the payroll process create this problem for themselves reliably, every December.

State tax treatment follows where the employee lives and works, not where the employer is headquartered. For multi-state employers and remote teams, this means recognition awards may be subject to state income tax rules in the employee's home state, which vary considerably. If your workforce spans multiple states, verify compliance with each state's supplemental wage rules rather than assuming federal treatment applies uniformly.

Where Recognition Programs Usually Break Down

Recognition compliance failures are surprisingly predictable. The same gaps appear across organizations of every size.

Gift cards distributed without W-2 reporting. This is the most common. There is no amount at which a gift card becomes tax-free. If your recognition policy includes gift cards going out without payroll coordination, it's generating liability right now.

Points programs launched without payroll integration. Redemption data that can't flow cleanly into payroll doesn't stay manageable. It accumulates until year-end, when it becomes a problem that is both urgent and entirely avoidable.

Peer-to-peer recognition treated as outside employer responsibility. The IRS doesn't care who initiated the award. If you fund and operate the platform, you own the reporting.

Using "recognition" framing to avoid withholding on what is functionally a bonus. The IRS evaluates substance, not labels.

The deeper pattern is that recognition programs tend to evolve faster than the operational processes around them. The program scales. The payroll integration doesn't. The year-end reconciliation is where that gap surfaces.

What to Ask Your Recognition Vendor

Tax compliance in recognition is not just a policy question. It's a platform capability question.

1. Can redemption data integrate directly into your payroll system, and in what format? A vendor who can't answer this specifically is leaving the integration work, and the compliance risk, with you.

2. Does the platform separate social recognition from monetarily-backed awards in its reporting? If everything runs through the same points ledger, your W-2 reconciliation will require manual intervention every single month.

3. Does the platform support a qualified §274(j) service award structure, and can it flag gift card redemptions separately? These aren't edge cases. They're the two categories where compliance errors are most common and most costly.

A platform that can't answer these questions is transferring compliance complexity back onto your team. That's a real operational cost that just doesn't show up in the pricing proposal.

On the business case: Why Employee Recognition Boosts ROI — and Why It Matters to You

The Rules, Plainly

For the CFO conversation, this is the one-page version.

- Cash and gift cards are always taxable. No minimum, no exception.

- Points become taxable at redemption, at the fair market value of what was received.

- Peer-to-peer recognition with monetary value creates employer W-2 obligations, regardless of who initiated the award.

- Service awards under §274(j) offer a real but narrow exclusion for tangible personal property, up to $1,600 under a qualified written plan.

- Social recognition with no monetary redemption value is never taxable.

The organizations getting this right aren't necessarily spending more on recognition. They're building programs that HR can scale, finance can defend, payroll can operationalize, and employees can trust. According to Gallup, only 22% of employees strongly agree they receive the right amount of recognition at work, which means the investment case is real. The question is whether the program is built to last or built to create a problem nobody notices until it's expensive to fix.

Recognition now sits at the intersection of culture, compensation, payroll, and compliance. Tax governance is no longer a footnote. It's what turns a morale initiative into sustainable organizational infrastructure.

A related pattern: Recognition Fatigue: Why Your Appreciation Program May Be Backfiring

Frequently Asked Questions

Are gift cards taxable income for employees?

Yes, always. The IRS treats gift cards as cash equivalents, fully taxable regardless of denomination, retailer, or occasion. There is no floor below which a gift card becomes tax-free. All must be reported as supplemental wages on the employee's W-2.

When do employee recognition points become taxable?

At redemption, not at accumulation. Under IRS guidance informed by Announcement 2002-18, unredeemed points create no tax obligation. The taxable amount is the fair market value of what the employee received at redemption, not the point balance they held.

What is the IRS limit for tax-free service awards?

$400 per employee per year under a non-qualified plan; $1,600 under a documented written plan. Under IRC §274(j), the award must take the form of tangible personal property, come after at least five years of service, with subsequent awards at least five years apart.

Are peer-to-peer recognition awards taxable?

It depends on monetary value. Social recognition with no redemption value is generally not taxable. The moment recognition carries redeemable economic value, it becomes taxable income. In all cases, the employer, not the nominating employee, owns the W-2 reporting obligation.

This article is written by Supriya Gupta. Supriya Gupta is a Content Marketing Lead at Vantage Circle, driving content strategy and thought leadership. She builds narratives that drive engagement and align brand purpose with impact.

Connect with Supriya on LinkedIn.